How to Read a Financial Aid Award Letter (2026 Guide)

If you are reading this in June, a stack of financial aid award letters is probably sitting on your kitchen table, and one of them needs an answer before the school's tuition deposit deadline rolls around in July or August. The frustrating part is that no two letters look alike. One school lists a grant as Estimated. Another bundles a federal loan into the same column as a scholarship and calls the total Aid Offered. A third quotes a number for the year that does not include the meal plan. The goal of this guide is simple: in about 15 minutes, you should be able to read any 2026-27 award letter, work out what the family is actually being asked to pay, and compare two or three offers on the same line.

Higher-education data team

Sources: Sourced from the U.S. Department of Education's Federal Student Aid program, the College Scoreboard institutional file, the National Association of Student Financial Aid Administrators (NASFAA), the College Cost Transparency Initiative, the Consumer Financial Protection Bureau's Paying for College tools, and the financial aid pages of more than thirty four-year U.S. colleges..

Why award letters are so hard to read

Award letters are the single most consequential document a college sends, and they are also the least standardized. A 2022 review by the U.S. Government Accountability Office found that 91% of colleges either understate or omit the net cost on their award letters, and about half include unsubsidized federal loans inside a total labeled aid. The Department of Education's voluntary College Financing Plan template was meant to fix this, but adoption is still partial.

What that means for a family in June 2026 is practical. The letter in your hand is probably designed to read as friendly. The real number, the one you write on a check or borrow against, is usually four or five subtractions away from the headline figure. Knowing where to look turns a 45-minute argument with a confusing PDF into a 15-minute decision.

The two numbers that actually matter

Strip an award letter down to its bones and you are looking for two numbers: cost of attendance and gift aid. Everything else on the page either rolls up into one of those, or it is a loan, which is not aid in any meaningful sense.

- Cost of attendance (COA). The full annual budget the school assumes a student will spend. It includes tuition and fees, room and board (or an off-campus housing estimate), books, personal expenses, and transportation. By federal definition, COA is the ceiling on how much aid you can receive.

- Gift aid. Money the student does not have to repay. Federal Pell Grants, state grants, institutional grants and scholarships from the school, and outside private scholarships all count. Gift aid is the only line that reduces the family's real cost.

- Self-help aid. Federal Direct Loans (subsidized and unsubsidized), Parent PLUS loans, and Federal Work-Study. These are options, not gifts. Loans become debt. Work-Study is a paycheck the student earns during the year and only if a job is available and worked.

- Net price. Cost of attendance minus gift aid only. This is the number to focus on. It is what the family will actually be asked to come up with through savings, current income, or loans.

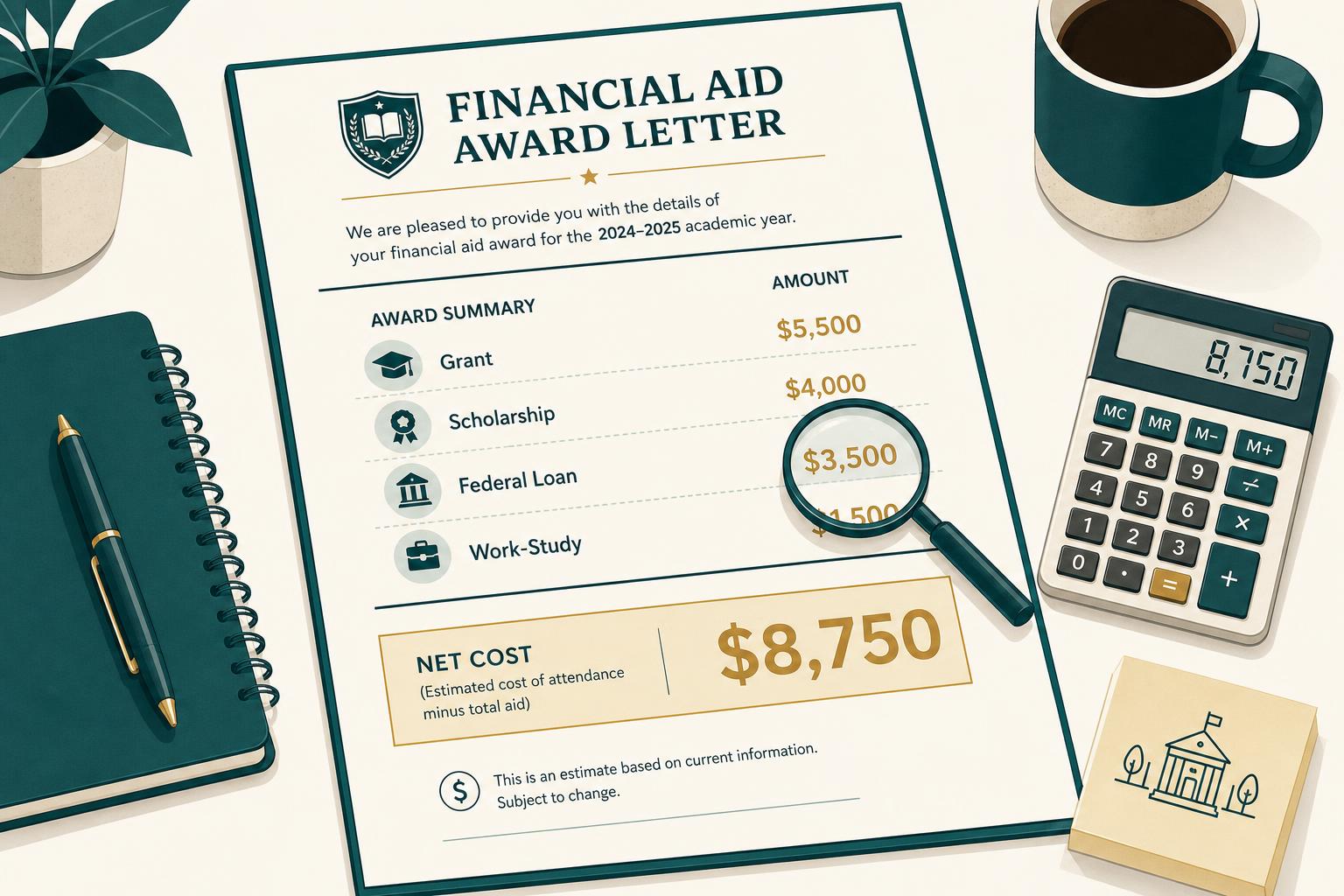

A line-by-line walkthrough of a 2026 award letter

Most award letters in 2026 follow one of three templates: the federal College Financing Plan, a homegrown school format, or a slightly cleaner version produced by schools that have signed on to the College Cost Transparency Initiative. Regardless of the template, you will find roughly seven rows. Read them in this order.

- Row 1: Cost of attendance for the year. Look for tuition and fees, housing and food, books, personal, transportation. If only tuition is listed, the school is showing direct costs only. Ask the financial aid office for the full cost of attendance figure or use the school's published budget on its financial aid page.

- Row 2: Grants from the school. Often called an institutional grant, university scholarship, founders award, or named scholarship. This is the line that most varies between schools and most often determines the answer.

- Row 3: Federal Pell Grant. Up to $7,395 for the 2026-27 award year for students with the highest demonstrated need on the FAFSA. If you see Pell on the letter and your FAFSA Student Aid Index (SAI) is in the eligible range, this is locked in.

- Row 4: State grant. State-level need-based programs (Cal Grant in California, TAP in New York, HOPE in Georgia, and so on) that the school includes when known.

- Row 5: Outside scholarships. Any private scholarships you have already reported to the school. These can sometimes reduce your institutional aid, a process called scholarship displacement; the school's policy on displacement is worth a direct question.

- Row 6: Federal Direct Loan, subsidized and unsubsidized. Up to $5,500 combined for first-year dependent students. Subsidized means no interest accrues while enrolled at least half-time; unsubsidized accrues interest from disbursement.

- Row 7: Federal Work-Study. A campus job award. It is paid as wages during the year, not credited to the bill, and the student has to find and work the job to receive it.

Doing the real math: net price in three steps

Once you have identified the seven rows above, the calculation is short. Use these three steps on every letter, even the ones that already print a 'You Pay' figure, because that figure often counts loans as aid.

- Step 1. Add only the gift aid lines: institutional grants and scholarships, Pell Grant, state grant, and outside scholarships. Do not include loans or Work-Study. The total is the family's true aid figure.

- Step 2. Subtract that gift aid total from the full cost of attendance figure in Row 1. The result is the school's real net price for the year.

- Step 3. Multiply by four (or by the realistic time-to-degree at that school) for the four-year picture. Then check the school's average graduation time, since paying net price for a fifth year is more common than families expect.

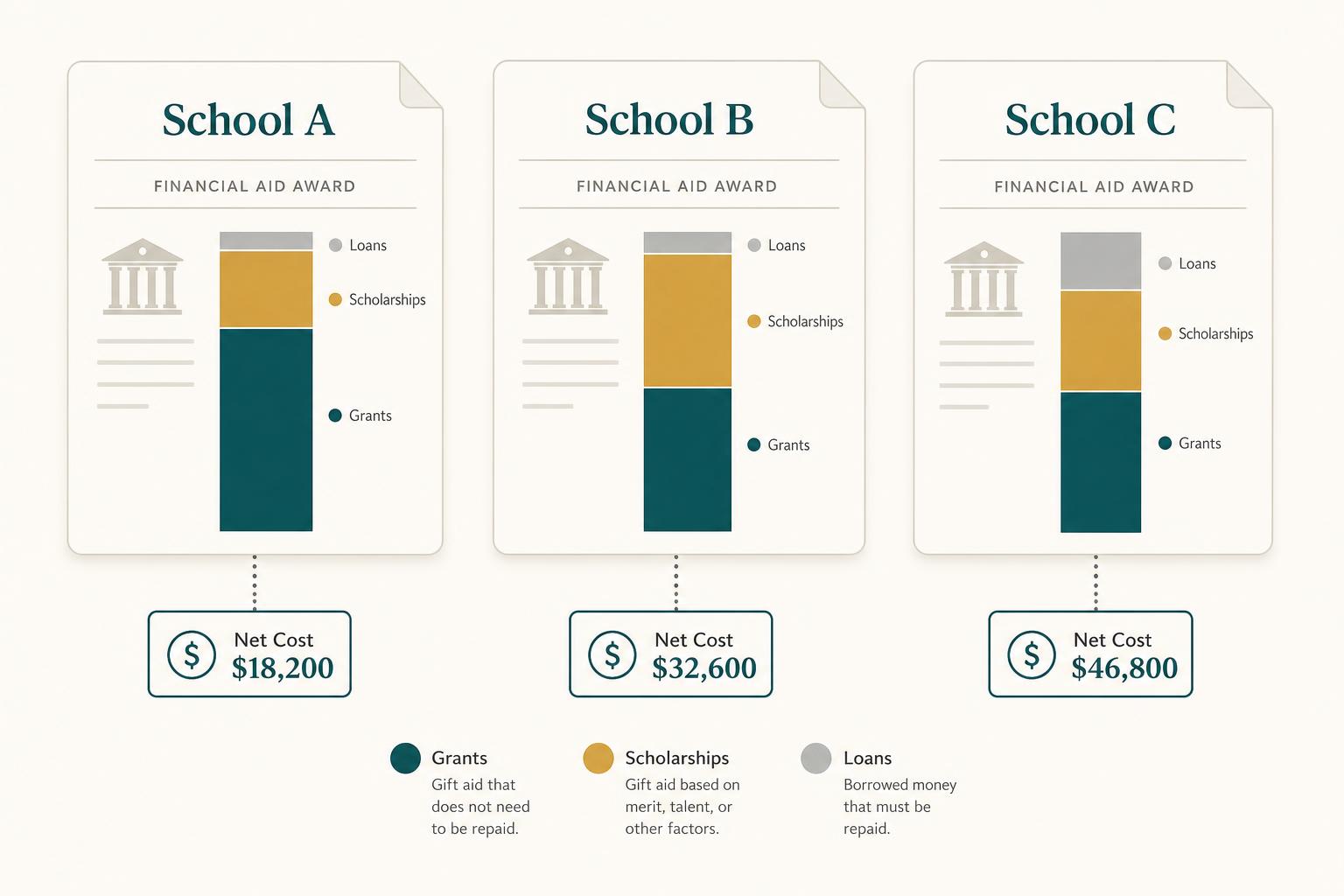

Comparing two or three offers on the same line

Award letters become easier the moment you stop reading them one at a time. Lay them side by side, use the same row labels for all of them, and force every school onto the same definitions. The free Paying for College tool from the Consumer Financial Protection Bureau will do this in a browser; a notebook page with three columns works just as well.

Be especially careful with three traps that show up almost every year in our reader questions.

- The off-campus housing trick. One school lists a $14,000 room-and-board figure; another lists $8,500 for off-campus rent and groceries. The off-campus number is almost always understated, and the family ends up paying the on-campus equivalent in cash.

- The first-year-only scholarship. A merit award labeled Founders Scholarship or Presidential Award may be a one-year award or may renew only if the student maintains a 3.4 GPA. Ask the financial aid office, in writing, whether the award renews and on what condition.

- Loans inside the 'aid' total. If a letter shows $32,000 of aid against a $50,000 cost of attendance, and the $32,000 includes a $5,500 Direct Loan and a $2,500 Work-Study, the real aid figure is $24,000 and the real net price is $26,000, not $18,000.

When and how to appeal an award

An aid appeal is not a negotiation in the retail sense, and using that word with a financial aid office is the fastest way to get a polite no. The accurate term is a professional judgment review. Federal law gives financial aid administrators authority to adjust the inputs to a student's aid calculation when there is a documented change in family circumstances that the FAFSA did not capture.

Grounds that financial aid offices actually act on are concrete and verifiable. A short, clear letter plus documentation is more effective than a long emotional appeal. Send it as soon as you have the documents, and copy a parent or guardian on the email so the school can verify the request is genuine.

- Job loss, reduced hours, or a permanent salary cut for a parent since the FAFSA was filed. Attach the termination notice or two recent pay stubs.

- A new medical bill or ongoing out-of-pocket medical expense not covered by insurance. Attach the explanation of benefits.

- A death or divorce in the immediate family. Attach the certificate or filing.

- A competing aid offer from a peer school, paired with a written request to be considered for a need or merit re-review based on that comparison. Some schools formally match peer awards; most consider them.

- Tuition or housing cost increases the school announced after the original letter was sent.

The 2026-27 financial aid calendar

Award letters do not exist in isolation. They tie into a sequence of FAFSA, verification, and bill-pay deadlines that runs from December through August. Knowing the rhythm tells you when to act on a letter and when to wait.

- December 1, 2025: 2026-27 FAFSA opens. Filing in December or January puts a family at the front of state grant queues, several of which run out of money on a first-come basis.

- March through April 2026: Selection for FAFSA verification. About one in four FAFSAs is selected. Respond quickly through the school's portal; verification holds delay aid disbursement.

- April through May 2026: Award letters arrive for admitted students. Most schools issue them within two to three weeks of an admission decision.

- May 1, 2026: National Candidates Reply Date. Most schools require a tuition deposit by this date, though many have shifted to June 1 for waitlisted or late-admit students.

- July through August 2026: First-semester bills go out, typically due 30 days before classes start. Any unfunded balance has to be covered by savings, monthly payment plan, or a loan.

What to do this week if you have a stack of letters

If the answer is due in the next 30 days and the letters are still confusing, work through this short list before deposit day. It will not make the choice easy, but it will make sure the choice is informed.

- Pull each school's full cost of attendance from its financial aid website. Do not rely on the bill the letter shows.

- Recalculate net price for each school using only gift aid. Write the four-year total next to it.

- List which scholarships renew automatically and which require a GPA or credit-hour minimum. Mark the schools where the first-year price is the lowest you will ever see.

- If any school's offer is more than $5,000 per year above the next-best peer school, draft a one-paragraph professional judgment review request. Email it before the deposit deadline.

- Run each school through a credible federal data source. Our school search and side-by-side compare tool pull verified net price, graduation rate, and median earnings data from the College Scorecard, so the family can see whether the school's outcomes match the price being asked.

Three quiet rules that save families money every year

Beyond the math, three habits show up again and again in families who end up paying less than the headline net price. They are not secrets, but they are not on most award letters either.

- Refuse the unsubsidized loan if the family can cover the gap without it. Subsidized loans are reasonable for many families; unsubsidized loans accrue interest from day one and the long-term cost compounds.

- Decline Work-Study only if the student is sure they will not work. Accepting it costs nothing if the job never materializes, and the wages do not count against next year's FAFSA the way ordinary earnings do.

- Submit the FAFSA for all four years, even if the family does not expect need-based aid. Many schools require a current FAFSA on file to renew institutional scholarships, and circumstances change.

Further reading

On UniScorecard

- How to read a college's net price

The longer explainer on net price vs sticker price, with worked examples.

- How to pay for college

The full plan: savings, current income, federal aid, and when borrowing makes sense.

- FAFSA 2026-27 deadlines

The filing calendar that feeds every award letter in your stack.

- How to compare colleges

Comparing schools on outcomes and price using federal data, not brochures.

- School search

Verified net price, graduation rate, and median earnings for every Title IV school.

- Side-by-side compare

Place two to four schools next to each other on the same financial line.

External sources

- Federal Student Aid: types of aid ↗

Official definitions for grants, loans, work-study, and scholarships.

- College Financing Plan template ↗

The Department of Education's voluntary standardized award-letter format.

- CFPB Paying for College ↗

Free side-by-side aid comparison tool from the Consumer Financial Protection Bureau.

- College Scorecard ↗

Federal data on net price, graduation rate, and median earnings by school.

- NASFAA: financial aid appeals ↗

Plain-language guidance from the National Association of Student Financial Aid Administrators.

- Federal Pell Grant program ↗

Eligibility and 2026-27 maximum award details.

Frequently asked

- What is the difference between gift aid and self-help aid on a financial aid award letter?

- Gift aid is money you do not repay: institutional grants and scholarships from the school, the federal Pell Grant, state grants, and outside scholarships. Self-help aid covers Federal Direct Loans (subsidized and unsubsidized), Parent PLUS loans, and Federal Work-Study. Only gift aid reduces the family's true net price; loans become debt and Work-Study is a paycheck the student earns.

- How do I calculate net price from a 2026-27 award letter?

- Add only the gift aid lines on the letter (institutional grant, scholarship, Pell Grant, state grant, outside scholarships). Subtract that total from the school's full cost of attendance figure, which includes tuition, fees, housing, food, books, personal expenses, and transportation. The result is the family's real net price for the year. Do not subtract loans or Work-Study from cost of attendance; they are not aid.

- Can a college financial aid offer be appealed in 2026?

- Yes. Federal law gives financial aid administrators authority to use professional judgment to adjust the inputs to a student's aid calculation when family circumstances have changed since the FAFSA was filed. Common grounds include job loss, salary reduction, new medical expenses, a death or divorce in the family, or a significantly stronger aid offer from a peer school. Submit a short written request with documentation through the school's financial aid portal.

- Why does one school's award letter look so different from another's?

- There is no federally required format for financial aid award letters. The U.S. Department of Education publishes a voluntary College Financing Plan template and the College Cost Transparency Initiative has published a standard format, but adoption is partial. Many schools still use a homegrown layout that bundles loans with grants under a single 'aid' total. To compare offers, copy each letter onto a single sheet with identical row labels: cost of attendance, gift aid, loans, work-study, and net price.

- When is the deadline to accept or decline financial aid for 2026-27?

- Most colleges require a tuition deposit by May 1, the National Candidates Reply Date. Many waitlisted or late-admit students have until June 1. The first-semester bill, which the family pays from a combination of savings, monthly payment plan, or accepted loans, is usually due in July or August, typically 30 days before classes start. The federal Direct Loan acceptance has a longer window and can be adjusted up to several weeks into the term.

About the author

UniScorecard Editorial

Higher-education data team

We translate the U.S. Department of Education's College Scorecard into plain-language guides for students, families, and counselors. Every metric we publish is sourced directly from the federal Most Recent Cohorts institutional file.

Read our methodology →